Cryptocurrency Tax Calculator

1 of 2

Table of content

- Cryptocurrency Tax Calculator

- Understanding Cryptocurrency Taxes

- How does it work?

- Crypto Sale and Exchange

- Cryptos are not treated as currency by IRS

- Cryptos are valued at the time of receipt of payment

- Mining cryptos and revenue recognition

- Mining cryptos & self-employment income

- Filing 1099 for payments to people who work for miners

- Salaries and wages paid in crypto are subject to W-2 requirements

- Filing 1099-MISC for payments made in cryptos

- Backup withholding for 1099 recipients

- Filing 1099-K for settlement payments made in cryptos

- Penalties for failure to comply with tax laws

- Is cryptocurrency subject to FBAR filing?

- Regulation of Cryptocurrency Initial Coin Offering (ICO)

Cryptocurrency Tax Calculator

Understanding Cryptocurrency Taxes

Cryptocurrency’s popularity continues to rise as coins such as Bitcoin, Ethereum, and alternate coins like Dogecoin and Shiba Inu continue to see their prices trend higher and higher.

For many across the country, cryptocurrency has transformed into an investing alternative, where investors can buy and sell at any time of the day and watch their money multiply throughout the year. Some prefer the coins over mainstream investments because cryptocurrency is decentralized. However, the IRS is still watching, looking to crack down on crypto tax compliance.

How Does It Work

For federal tax purposes, cryptocurrencies or virtual currencies are seen as ‘Property’ and the IRS treats them as capital assets. So, any transactions concerning cryptocurrencies are governed by the same tax principles applied to “Property” as per IRS Publication 544, Sales and Other Dispositions of Assets.

When you sell virtual currency, you must recognize any capital gain or loss on the sale, subject to any limitations on the deductibility of capital losses. Your gain or loss will reflect the difference between your adjusted basis in the virtual currency and the amount you received in exchange for the virtual currency, which you must report on your income tax return in U.S. dollars.

The process of calculating your crypto taxes can seem complicated, which is why it is better to rely on an A.I-powered crypto tax calculator like FlyFin.

Crypto Sale and Exchange

According to the IRS, a sale is described as a transfer of property for money or a mortgage, or another promise to pay money, while an exchange refers to a transfer of property for other property or services.

If you sell your Ethereum (blockchain platform with its cryptocurrency) and receive US dollars in payment, it will be considered a “sale”. However, if you sell your Ethereum and receive Bitcoin as compensation, it will be considered an “exchange”. Both examples are related to “taxable” income.

Check out the following examples to understand the crypto capital gains tax:

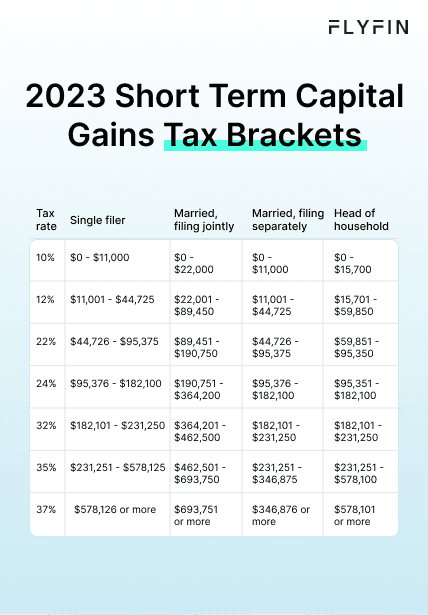

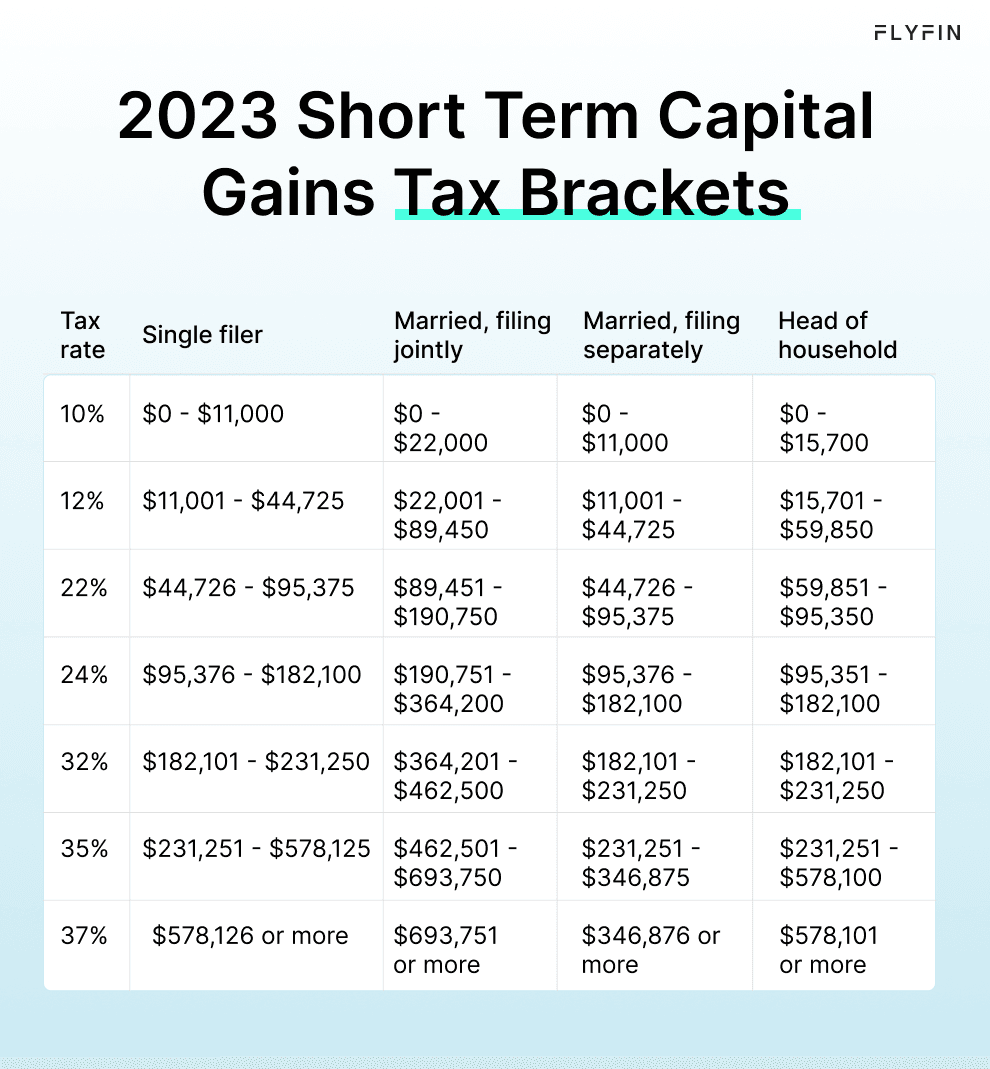

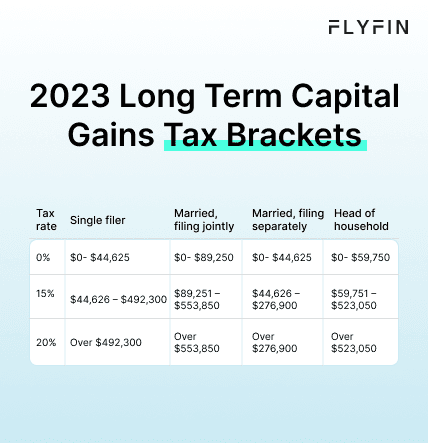

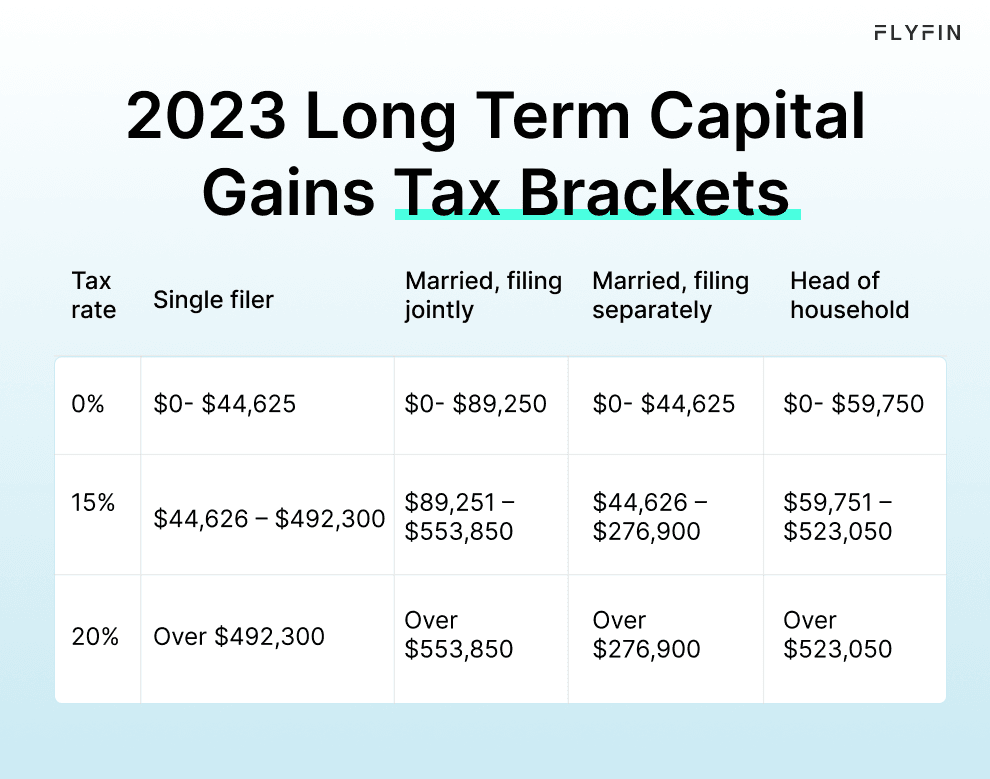

Example 1: On July 26, 2018, you sold your crypto for $500, and had purchased it on February 3, 2017, for $100. Here you will have $400 long-term capital gains because you kept the crypto as a capital asset (stocks, bonds, and other investment property are generally capital assets) for more than one year.

Selling Price: $500

Cost of Purchase: $100

Long-Term Capital Gains: $400

Example 2: Continuing with the same example above, if you had acquired the crypto on November 15, 2017, for $400, then you will have a $100 short-term capital loss.

Selling Price: $500

Cost of Purchase: $400

Short-Term Capital Loss: $100

Example 3: Example 3: Now, suppose you exchanged the Bitcoin that you had purchased on March 2, 2017, for $100, for Ethereum with a fair market value of $400. You will have $300 long-term capital gains.

Selling Price: $400

Cost of Purchase: $100

Long-Term Capital Gains: $300

Note: If the calculation seems too confusing, try using the crypto gains tax calculator.

Cryptos are not treated as currency by IRS

As per the current tax law, cryptocurrency is not considered a valid form of “currency,” and as a result, IRC Section 899 doesn’t apply to it. However, under Section 988(a) (1), a taxpayer’s foreign currency gain or loss is calculated separately and treated as ordinary income or loss rather than capital gains or losses.

Payments made in crypto for the sale of goods and services are income

People who receive cryptocurrency as payment for the sale of their goods and services must include the US dollar’s fair market value at the time of its receipt in the determination of their revenue.

Taxes on crypto: for income tax purposes, the basis of cryptocurrency that a taxpayer receives as payment is based on the US dollar’s fair market value on the date of its receipt.

Cryptos are valued at the time of receipt of payment

For the cryptocurrency listed on an exchange platform like Coinbase, the exchange rate is set by market supply and demand. It will be converted into the value of US dollars that it is worth at the time.

Mining crypto and revenue recognition

The process where a taxpayer uses high-tech computers to validate cryptocurrency transactions while maintaining a public transaction ledger is called mining. According to the law, the fair market value of the cryptocurrency mined, as of the date of receipt, should be included in the taxpayer’s gross income.

As per AICPA’s proposal, revenue recognition should be postponed until the product is sold or exchanged. However, the proposal has not been adopted yet.

Mining crypto & self-employment income

Self-employed taxpayers who mine cryptocurrency as a trade or business, have to pay both income taxes and self-employment taxes (Social Security and Medicare) on their net income.

These miners are treated as self-employed taxpayers, and are eligible to deduct the following business expenses:

- Cost of goods sold

- Travel expenses tax deduction

- Mileage tax deduction

- Insurance tax deduction

- Rent tax deduction

- Salaries paid to independent contractors

- Pension plans

- Self-employed home office deduction

- Deprecation of business equipment

Use the cryptocurrency tax calculator to figure out the type of tax deductions you can claim.

Filing 1099s for payments to people who work for miners

Taxpayers who work as independent consultants for other taxpayers who mine cryptocurrencies are also treated as self-employed taxpayers, and their net income from their trade or business is subject to both income tax and self-employment taxes. This applies whether or not they receive their compensation in US dollars or Bitcoin, Ethereum, Bitcoin Cash, Cardano (ADA), Litecoin, Dogecoin, BAT, NEO, Ripple XRP, Stellar (XLM), or any other kind of cryptocurrency.

Salaries and wages paid in crypto are subject to W-2 requirements

Similarly, any compensation paid to a W-2 employee in the form of cryptocurrency is subject to federal income tax withholding, which includes Social Security tax, Medicare tax, Federal Unemployment Tax Act (FUTA), and state withholdings. All this must be reported on Form W-2, Wage, and Tax Statement.

Filing 1099-MISC for payments made in cryptos

Any business transactions using cryptocurrency are subject to the IRS information reporting obligations to the same extent as US dollars or any other property.

Therefore, when the fair market value of the cryptocurrencies used for paying salaries, rents, insurance premiums, and other independent contractors’ compensations for rendering services is determined to be $600 or more in a taxable year, the taxpayer is required to report them to the IRS Form 1099-MISC, as Miscellaneous Income. It should be noted that the recipients of the value of $600 should report their income even if they do not receive a Form 1099-MISC.

Recipients cannot exclude the value of benefits from their income just because they didn’t receive a Form 1099-MISC.

Backup withholding for 1099 recipients

Any payments made to a non-W-2 individual with cryptocurrency are subject to backup withholding to the same extent as payments made using US dollars or any other property.

According to IRS Form 1099-MISC, payers making payments of $600 or more in a calendar year, using cryptocurrencies, are required to ask for a TIN from each payee.

As per the IRS Form 1099-MISC instructions, the payers must backup withholding from payments if:

- No TIN was obtained before making the payments or

- Payers receive notification from the IRS that backup withholding is required.

Filing 1099-K for settlement payments made in cryptos

A third party, such as a credit card company that negotiates with a substantial number of unrelated merchants to settle payments between the merchants and their customers, is called a third-party settlement organization (TPSO).

A TPSO must report payments made to a merchant on an IRS Form 1099-K, Payment Card, and Third-Party Network Transactions, if, for the calendar year, both the merchant:

- Settles over 200 payments; and,

- Payments exceed $20,000.

When completing the following boxes on 1099-K:

- Box 1a, Gross Payments

- Box 1b, Card Not Present Transactions

- Box 3, Number of Payment Transactions

- Box 5a through 5l, Payments During January through December

Transactions, where the TPSO settles payments made with cryptocurrencies, are aggregated with the payments made with US dollars, and other property to determine the total amounts to be reported in those boxes.

The value of the cryptocurrencies is the fair market value of it in US dollars at the date of payment.

Penalties for failure to comply with tax laws

When it comes to taxes on crypto gains, taxpayers may be subject to non-compliance penalties using cryptocurrency, the same as using US dollars and other property. Penalties include, but are not limited to

- 20-40% for accuracy-related errors, under § section 6662

- 0.05% per month up to 25% for failure to file a tax return under §6651(a)(1)

- Failure to pay taxes penalty of 0.5% per month up to 25%, under §6651(a)(2)

- Civil fraud of 75%

- $10K for failure to non-willfully file FBAR, per account, per year

- $100K or 50% for willfully failing to file FBAR

- Criminal prosecution for willful failure to file FBAR

- $10K for failure to file FATCA Form 8938 up to $50K

Is cryptocurrency subject to FBAR filing?

Although the IRS doesn’t recognize cryptocurrency as “currency”, some tax attorneys believe cryptocurrencies are subject to FBAR filing, because they function as fiat money and appear like “financial assets”.

Moreover, it is advised to file FBAR when in doubt.

But, the BSA Compliance Department claims that digital currency like Bitcoin can only be FBAR reportable if it is held in an account with a “financial institution” or someone acting as a “financial institution”.

Since digital currency is held in a “digital wallet”, not in a financial institution, it is not reportable on FBAR , because the digital wallet is not a recognized foreign financial account.

Regulation of Cryptocurrency Initial Coin Offering (ICO)

As per the following report, Cryptocurrency ICOs are regulated by the Securities and Exchange Commission (SEC):

The report emphasizes the fundamental principles of the U.S. federal security laws and details their applicability to a new paradigm of virtual organizations or capital raising entities that use a distributed ledger or blockchain technology to facilitate investment and sale of securities.

The automation of certain functions through this technology, ‘smart contracts,’ or computer code, does not remove conduct from the purview of the U.S. federal securities laws.

Stop estimating and start calculating your crypto tax using an A.I calculator

Taxes are complicated, crypto tax isn’t any different. As the industry evolves, the IRS too modifies and amends its tax code regarding cryptocurrency. But avoiding or neglecting to report your cryptocurrency gains, losses, and income on your taxes is considered tax fraud by the IRS.

It can lead to a steep penalty of up to $250,000 along with criminal prosecution and five years in prison. The IRS has admitted to sending out letters to crypto investors they believe are underreporting or evading tax. So, if you possess cryptocurrency by earning, trading, or selling it, make sure to report it on your tax return.

If the process of filing crypto taxes seems too complex, hire a CPA or try FlyFin’s Crypto Tax Calculator. It helps you determine your cryptocurrency tax based on the following information:

- Your tax filing status

- Your annual freelancing income

- Your crypto transactions

Plus, the cryptocurrency tax calculator is backed by CPAs who are available to assist you to calculate crypto taxes.

Frequently Asked Questions

Do you have to pay taxes on crypto?

How is crypto taxed?

Can a musician deduct the cost of a Spotify subscription?

Can these deductions help in lowering my tax liability?

How are crypto gains taxed?

How do you avoid taxes on crypto?

What is the short-term crypto capital gains tax rate?

What is the long-term crypto capital gains tax rate?

How does FlyFin’s crypto tax calculator help handle crypto tax?

How much is crypto taxed?

FlyFin’s got your back!

A.I. finds every tax deduction eliminating 95% of your work

Expert tax CPAs ensure 100% accurate tax filing

On average users save $3,700